Texas Closing Costs 2026: Fees & Savings

CEO & Founder of Chestnut Mortgage. NMLS #2687968. · May 11, 2026

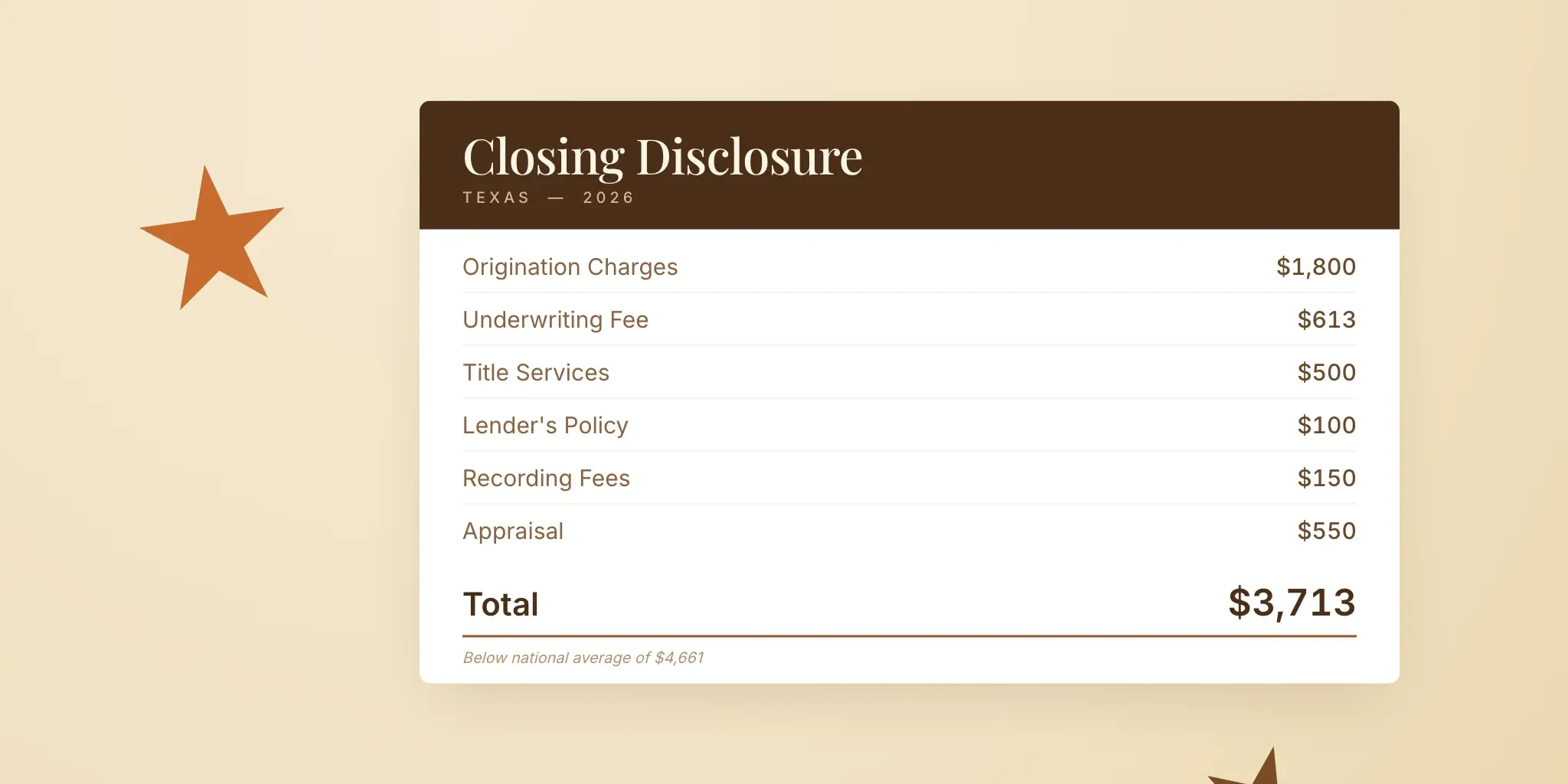

Texas homebuyers pay an average of $3,713 in closing costs, about 0.93% of the home sale price. That is meaningfully lower than the national average of $4,661 (1.6%) and dramatically lower than New York ($13,738) or Washington D.C. ($17,545).

Why so much cheaper? Texas has no state transfer tax, title insurance rates are tightly regulated, and refinances inside eight years of purchase qualify for substantial title insurance discounts. Those structural advantages can save you thousands, but only if you know to ask for them.

Here is exactly what you can expect to pay at a Texas closing in 2026, where the savings hide, and how to push the total lower.

What closing costs cover on a Texas mortgage

Closing costs are the fees you pay to finalize the loan and transfer the property. The Consumer Financial Protection Bureau requires lenders to itemize them on your Closing Disclosure, which arrives three business days before you sign.

Texas closing costs fall into five categories that show up on every Closing Disclosure.

Lender charges

These are fees Chestnut or any other lender charges for originating, underwriting, and funding your loan.

| Fee | Typical range | What it covers |

|---|---|---|

| Origination fee | 0.5% to 1% of loan | Processing and funding the loan |

| Underwriting fee | $300 to $750 | Income, credit, and risk review |

| Processing fee | $300 to $900 | Moving the file through closing |

| Credit report | $35 to $75 | Tri-merge credit pull |

| Discount points (optional) | 0% to 2% of loan | Buying down the interest rate |

On a $350,000 Texas loan, lender charges typically run $1,500 to $5,000 before any discount points.

Services you can shop for

The CFPB requires lenders to tell you which services you can shop for and which they require. In Texas, that almost always includes title insurance and the title closing fee, sometimes the survey, and pest inspection.

Shopping these services can save real money. A title agency that quotes $400 for a closing fee instead of $750 keeps $350 in your pocket.

Services your lender selects

Appraisal, flood certification, and the credit report typically come from vendors your lender chooses. These run $500 to $750 on a standard single-family Texas appraisal, more for rural properties or unique homes.

Taxes and government fees

This is where Texas saves you money. Most states charge a transfer tax of 0.5% to 2% on the sale price. Texas has no state-level transfer tax, and the only government fees at closing are recording fees, typically $20 to $200 per document depending on the county.

Prepaids and escrow

Even though they appear at closing, prepaids are not really closing costs. They are amounts you would owe anyway, just collected upfront:

- Prepaid interest from closing date to month-end

- First year of homeowners insurance

- Property tax reserve (Texas property taxes run high, so this can be the biggest line on the page)

- Initial escrow deposit (usually 2 to 3 months of taxes and insurance)

Texas has the seventh-highest effective property tax rate in the nation at 1.40% of owner-occupied home value according to the Tax Foundation. A $400,000 home means roughly $5,600 per year in property taxes, so your escrow reserve at closing (typically 2 to 3 months of taxes and insurance) can easily exceed $1,500.

Texas title insurance: promulgated rates and refi discounts

Title insurance is the single biggest third-party cost on most Texas closings, and Texas regulates it differently than almost any other state.

How promulgated rates work

The Texas Department of Insurance sets the title insurance rate schedule by Commissioner’s order. As of March 1, 2026, every Texas title agent must charge the same basic premium for a policy of a given size. Shopping for a lower title insurance premium is impossible in Texas because the rate is regulated, not market-driven.

The basic premium rates for owner’s title insurance, effective March 1, 2026:

| Policy amount | Basic premium |

|---|---|

| $25,000 | $308 |

| $50,000 | $465 |

| $100,000 | $780 |

| $250,000 | $1,521 |

| $500,000 | $2,757 |

| $750,000 | $3,992 |

| $1,000,000 | $5,228 |

For policies above $100,000 the formula is $780 plus 0.494% of the amount above $100,000, scaling down at higher tiers. The TDI publishes the full rate schedule with worked examples.

The refinance discount most Texans miss

This is the single most underused savings opportunity in Texas closings. Under TDI Rate Rule R-8, refinancing within eight years of buying your home qualifies for a substantial title insurance discount:

- Refinance within 4 years of purchase: 50% off the basic premium (R-8.B.1)

- Refinance 4 to 8 years after purchase: 25% off (R-8.B.2)

On a $350,000 refinance two years after purchase, the lender’s policy basic premium is roughly $2,015. The 50% R-8.B.1 discount drops that to about $1,008, saving you roughly $1,007 at closing. Title agents do not always apply this discount automatically. Bring your original Closing Disclosure to your refi closing and ask for the rate reduction in writing.

The 2% fee cap on Texas refinances

Texas Finance Code Chapter 343 caps total fees on certain Texas home loans, including most home equity loans and cash-out refinances, at 2% of the loan amount. The cap excludes third-party costs like title insurance, appraisal, and recording fees, but it sharply limits what your lender can charge for origination, underwriting, and processing.

Chestnut’s Texas refinance flow keeps lender fees well under the cap by default. If you are shopping a Texas cash-out refi or home equity loan and your lender’s fees look like they exceed 2% of the loan, ask which fees are included and which are not.

Who pays what at a Texas closing

Unlike states with rigid customs, Texas leaves most cost allocation to negotiation in the purchase contract. The TREC (Texas Real Estate Commission) one-to-four family residential contract is the default, and it spells out who pays each line item.

Typical Texas allocation under the standard TREC contract:

| Fee | Buyer | Seller |

|---|---|---|

| Owner’s title insurance | X | |

| Lender’s title insurance | X | |

| Title closing fee | Negotiable, often split | Negotiable, often split |

| Survey | Negotiable | Often seller |

| Appraisal | X | |

| Lender origination | X | |

| Recording fees | X | |

| HOA transfer fee | Negotiable | Negotiable |

| Property tax proration | X (going forward) | X (year to date) |

The seller paying the owner’s title policy is a Texas convention worth millions to buyers cumulatively. In states like California, the buyer pays for both policies.

See your rate in 2 minutes

No phone calls. No credit check. Compare options from 100+ lenders.

Email ChestnutReal cost scenarios by loan size

These scenarios estimate total closing costs for a Texas conventional purchase, assuming 20% down, average lender fees, and standard title and escrow costs. They do not include prepaid property taxes or homeowners insurance.

In a Texas purchase, the seller pays the owner’s title insurance policy under the standard TREC contract. The buyer pays a lender’s title policy, which is $100 at simultaneous issue per TDI Rate Rule R-3. That single Texas convention is the main reason buyer closing costs here run thousands below most other states.

$200,000 loan ($250,000 home)

| Category | Estimated cost |

|---|---|

| Lender fees | $1,800 |

| Appraisal | $550 |

| Lender’s title policy (simultaneous issue) | $100 |

| Title closing fee | $400 |

| Survey | $500 |

| Recording fees | $150 |

| Estimated buyer total | $3,500 |

$400,000 loan ($500,000 home)

| Category | Estimated cost |

|---|---|

| Lender fees | $3,200 |

| Appraisal | $600 |

| Lender’s title policy (simultaneous issue) | $100 |

| Title closing fee | $450 |

| Survey | $550 |

| Recording fees | $200 |

| Estimated buyer total | $5,100 |

$600,000 loan ($750,000 home)

| Category | Estimated cost |

|---|---|

| Lender fees | $4,800 |

| Appraisal | $700 |

| Lender’s title policy (simultaneous issue) | $100 |

| Title closing fee | $500 |

| Survey | $600 |

| Recording fees | $250 |

| Estimated buyer total | $6,950 |

These totals exclude prepaid property taxes, homeowners insurance, and the seller-paid owner’s title premium. Buyer totals scale much more flatly than loan amount in Texas precisely because the seller absorbs the owner’s premium and the buyer’s lender policy is fixed at simultaneous issue.

Your actual costs will vary based on lender, county, and loan type. Chestnut’s Texas refinance break-even guide walks through how to evaluate whether refinancing into a higher rate still makes sense given specific closing cost math.

How to lower your Texas closing costs

Even with Texas’s structural advantages, there is meaningful room to cut your total. Five strategies that actually work:

1. Get lender credits in exchange for a slightly higher rate. If you plan to stay under five years or expect to refinance soon, taking a 0.125% higher rate in exchange for $2,000 in lender credits often comes out ahead. Run the breakeven before deciding.

2. Shop title and escrow services. Texas title insurance rates are regulated, but title agents compete on closing fees, document prep fees, and courier fees. Ask three title agencies for a quote on the same policy and you will often see $300 to $700 in variance on non-premium charges.

3. Ask the seller for closing cost concessions. Texas contracts allow sellers to credit up to 3% of the home price toward buyer closing costs on conventional loans, up to 6% with FHA. In a soft market, this is regularly negotiated.

4. Refinance within eight years to capture the title discount. If you bought a home in 2018 to 2022 and are now considering a refi, confirm with the title company that the 50% or 25% discount applies to your timeline.

5. Compare lender APRs, not just rates. APR rolls closing costs into the borrowing cost so two loans with the same headline rate can have very different APRs. Comparing APRs is the cleanest single way to spot a high-fee lender.

How Colorado closing costs compare

Colorado homebuyers pay an average of $3,895 in closing costs, roughly 0.92% of the sale price, almost identical to Texas. The main differences:

- Colorado has a 0.01% real estate transfer tax (negligible) where Texas has none

- Colorado does not regulate title insurance rates; you can shop title premiums in CO but not in TX

- Colorado has no equivalent to the Texas 2% fee cap on cash-out refinances or home equity loans

For Chestnut borrowers in both states, the closing cost gap is small. The bigger structural differences show up in Texas Section 50(a)(6) home equity rules, where the constitutional 80% LTV cap, 2% fee ceiling, and 12-day cooling-off period create stricter limits than anything in Colorado.

More Texas mortgage guides

- Refinancing a 4% Texas Mortgage: Break-Even Math

- Mortgage Closing Costs Explained: Fees, Payers, Savings

- HELOC vs Home Equity Loan: Which Is Right for You

- Lowest Closing Costs Mortgage Lender: 2025 Comparison

- 5 Ways Chestnut Streamlines the Home Purchase Process

Frequently Asked Questions

How much are closing costs on a $400,000 house in Texas?

Buyer closing costs on a $400,000 Texas home with a $320,000 loan typically run $4,500 to $6,000 in fees, plus prepaid property taxes and insurance. The seller pays the owner’s title policy. The buyer’s lender’s policy is $100 at simultaneous issue per TDI Rate Rule R-3, and lender fees usually add $2,000 to $3,500.

Does Texas have a transfer tax at closing?

No. Texas is one of about 13 states with no real estate transfer tax. The only government fee at a Texas closing is the county recording fee, usually under $200 per recorded document.

Why is title insurance the same price at every Texas title company?

The Texas Department of Insurance promulgates the basic premium rate schedule by Commissioner’s order. Every title agent must charge the same premium for a policy of a given amount. Title agents compete on closing fees, document prep, and courier fees, so the full title bill can still vary by a few hundred dollars.

Who pays closing costs in a Texas home sale?

Allocation is negotiable in the purchase contract, but the TREC standard contract defaults to the seller paying the owner’s title policy and the buyer paying the lender’s title policy, the appraisal, and most lender fees. Sellers can credit up to 3% of the home price toward buyer closing costs on conventional loans.

Can I roll closing costs into my Texas mortgage?

On a purchase, no, you generally cannot finance closing costs into a Texas mortgage. On a refinance, yes, you can roll closing costs into the new loan balance, increasing your loan amount by the cost amount. The math only works if your new rate is low enough to absorb the higher balance.

When do I get my Texas Closing Disclosure?

Federal rules require lenders to deliver the Closing Disclosure at least three business days before signing. Use that window to compare it line by line against your most recent Loan Estimate. Anything that changed materially is worth a phone call to your loan officer.

What is the Texas 2% fee cap and does it apply to my loan?

Texas Finance Code Chapter 343 caps lender and broker fees at 2% of the loan amount on most Texas home equity loans and cash-out refinances. It does not apply to standard purchase mortgages or rate-and-term refinances. Third-party fees like title insurance and appraisal are excluded from the cap.

Sources

- Bankrate, Average Closing Costs By State, 2025

- Consumer Financial Protection Bureau, Closing Disclosure Explainer

- Texas Department of Insurance, Title Insurance Rates Effective March 1, 2026

- Texas Department of Insurance, Title Insurance Home

- Texas Department of Insurance, Basic Manual of Title Insurance Section III - Rate Rule R-8

- Texas Finance Code, Chapter 343 - Home Loans

- Tax Foundation, 2026 Texas Tax Rates and Rankings

- Texas Real Estate Commission, Standard Forms

Sources

Data and statistics referenced in this article are sourced from public mortgage industry reports and Chestnut's internal analysis.

Ready to find

your best rate?

Our automated quote flow is paused. Email contact@chestnutmortgage.com and the Chestnut team will help directly.