Rate Jumped? Switch Lenders in Aurora CO

CEO & Founder of Chestnut Mortgage. NMLS #2687968. · May 7, 2026

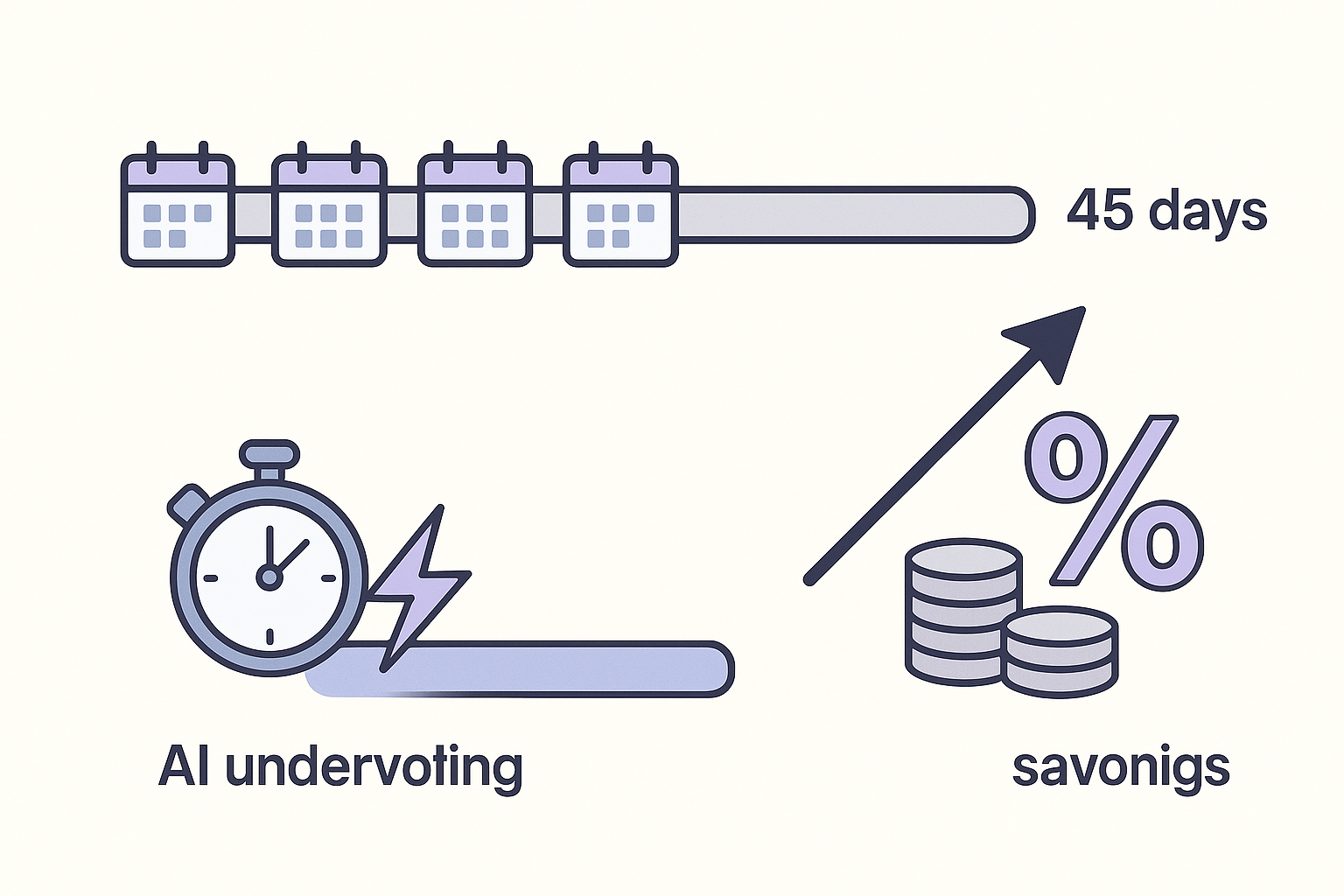

Colorado law protects your right to switch mortgage lenders anytime before signing final loan documents, even mid-process. Switching typically takes 30-45 days with traditional lenders, but Aurora borrowers can leverage AI-powered platforms like Chestnut that compress underwriting to just eight minutes. This speed advantage becomes critical when facing rate jumps, as Chestnut’s technology cuts rates by approximately 0.5% while maintaining closing timelines.

At a Glance

• You can legally switch lenders at any point before signing final loan documents in Colorado • Expect duplicate costs like appraisals ($800-$950) and credit reports ($25-$50) when switching • AI-based underwriting reduces processing from 30-45 days to eight minutes • Complete all lender applications within a short window to minimize credit score impact • Aurora’s 122% decrease in home affordability since 2013 makes rate optimization essential • Chestnut’s AI compares over 100 lenders simultaneously to find optimal rates

A sudden rate spike in the middle of your home purchase can feel like the floor dropping out. You have been counting on one number, and now a new, higher one threatens to blow your budget or derail the deal altogether. The good news is that you are not locked in until you sign final loan documents. This guide walks through how to switch mortgage lenders in Aurora CO quickly, what Colorado regulations protect you, and how Chestnut’s AI-powered platform can compress a typically weeks-long process into minutes.

Sudden Rate Jumps: Why Aurora Borrowers Consider Switching Mid-Process

Mortgage interest rates can change daily, sometimes more than once. If you started your application when rates were lower and watched them climb before closing, you are facing a real cost increase on a loan you will carry for decades.

The current mortgage rate volatility index stands at 102.20, indicating moderate fluctuation that savvy borrowers can leverage with proper timing strategies. That volatility cuts both ways: it creates opportunity, but it can also leave you scrambling when your quoted rate expires or jumps unexpectedly.

“If you’re having a bad experience with a mortgage lender, you may be tempted to switch to a different one before you close on the loan,” notes WTOP. Common triggers for switching include:

- Delays to the closing date

- Poor customer service or constant staff turnover

- Unexpected changes in loan fees or terms

- A lower rate available elsewhere

Understanding how mortgage rates work is the first step toward regaining control when the numbers move against you.

How do rate locks and float-downs protect Colorado borrowers - and when do they fail?

A rate lock is your shield against market swings. Locking your interest rate means the rate and any associated points are guaranteed for the lock period, protecting you from market fluctuations.

Not every lock, however, accounts for a market downturn after you commit. That is where a float-down option comes in. A float-down option could allow a one-time interest rate reduction if market rates fall after you lock a rate with a lender. It offers flexibility, but there are trade-offs:

| Feature | Standard Rate Lock | Float-Down Option |

|---|---|---|

| Protection against rising rates | Yes | Yes |

| Benefit from falling rates | No | Yes (one-time) |

| Upfront fee | Typically none | Often 0.25% to 1% of loan |

| Availability | Universal | Varies by lender |

Float-down fees typically range from 0.25% to 1% of the total loan amount. Whether the fee pays off depends on how far rates drop and how long you hold the loan.

As of May 2026, Chestnut Mortgage offers a 30-year fixed rate of 5.605% (5.645% APR), while major lenders range from 5.875% to 6.75%. Borrowers who locked at peak rates last year are now exploring refinancing or switching mid-deal to capture lower pricing. If your current lender does not offer a float-down, or you missed the window to use it, switching may be your best path to a better rate.

You can compare rates side-by-side to see whether a switch pencils out.

See your rate in 2 minutes

No phone calls. No credit check. Compare options from 100+ lenders.

Email ChestnutCan Colorado borrowers legally switch lenders before closing?

Yes. “You can switch mortgage lenders at any time before you sign the contract for a mortgage loan,” confirms U.S. News. “As the borrower, you have the right to switch mortgage lenders at any time before you sign the loan contract,” echoes WTOP.

Colorado adds another layer of oversight. The Secure and Fair Enforcement for Mortgage Licensing Act of 2008 was enacted to increase uniformity and enhance consumer protection. All mortgage loan originators in the state must be licensed through the Nationwide Mortgage Licensing System and Registry, and the Division of Real Estate investigates complaints on behalf of borrowers.

Key takeaway: Federal and Colorado law both protect your right to shop or switch lenders right up until you sign final loan documents.

What happens to your loan servicing after a switch?

If you switch lenders, you may also experience a servicing transfer where the company collecting your monthly payments changes. Here is what the Consumer Financial Protection Bureau requires:

- Your old servicer generally should send notice at least 15 days before the transfer.

- Your new servicer generally should send a notice within 15 days after the transfer.

- For 60 days from the transfer date, your new servicer cannot charge late fees if you accidentally sent payment to your old servicer on time.

These built-in safeguards mean a switch does not have to create payment confusion.

Five Steps to Switch Mortgage Lenders Fast in Aurora

Speed matters when your closing date is already on the calendar. Here is a streamlined checklist:

-

Confirm your timeline. Calculate how many days remain until your scheduled closing. Switching adds steps, but AI-powered lenders can offset much of that delay.

-

Gather your documents. “You’ll need to submit a new application and undergo another credit check from the new lender,” notes WTOP. Having pay stubs, tax returns, and bank statements ready prevents delays.

-

Shop multiple lenders in a tight window. Complete all mortgage applications within a short timeframe so credit bureaus can group inquiries together, minimizing score impact.

-

Get a rapid pre-approval. Chestnut delivers fully documented pre-approval letters in under two minutes through proprietary AI-powered underwriting, compared to 6 to 10 days at traditional banks.

-

Coordinate with your real estate agent and title company. Let them know the lender is changing so they can update wiring instructions and document routing.

“AI-based underwriting reduces the mortgage application processing time from an average of 30-45 days to just eight minutes,” reports Chestnut. That speed can save a deal that would otherwise slip past your closing deadline.

For a deeper dive on preparation, see 5 steps to get preapproved fast.

Document checklist & credit-pull tips

Switching lenders means resubmitting paperwork. Keep these items organized:

- Last two years of W-2s or 1099s

- Most recent 30 days of pay stubs

- Two months of bank statements

- Government-issued ID

- Current mortgage statement (if refinancing)

“You’ll need to submit a new application and undergo another credit check,” explains U.S. News. To protect your credit score:

- Complete all lender applications within a short window so inquiries are bundled.

- Avoid opening new credit accounts during the process.

Appraisals can be a sticking point. Depending on how far you have gotten in the mortgage process, you may need to repeat some costs you have already paid. Some lenders accept appraisal transfers; ask upfront to avoid a duplicate fee.

“If a new appraisal is needed, there is a risk that the value of the home could come back lower than the original appraisal, which could negatively impact pricing, product and other factors.” - U.S. News

What fees and delays should you expect when switching lenders in Aurora?

Switching is not free. Understanding the potential costs helps you weigh whether a lower rate justifies the effort.

| Cost Category | Typical Range in Colorado |

|---|---|

| Home appraisal (if new one required) | $800 to $950 |

| Credit report fee | $25 to $50 |

| Rate-lock extension (if needed) | Varies; often 0.125% to 0.25% of loan per week |

| Title update/re-issue | $100 to $300 |

A Freddie Mac study found that buyers who got quotes from at least four lenders saved up to $1,200 annually. Over a 30-year loan, those savings compound significantly, often dwarfing the one-time costs of switching.

Beyond fees, time is the hidden cost. “Switching to a different lender could delay your closing timeline, which could impact your deal,” warns WTOP. If you have a contractual closing date, missing it may expose you to penalties or risk losing the home.

Key takeaway: Run the numbers. If the rate savings over the life of the loan exceed the upfront switching costs and you can meet your timeline, a switch usually makes financial sense.

Why Chestnut cuts days and basis points in Aurora

“Chestnut is the first AI mortgage lender. We automate 99% of human work with AI agents, saving customers 0.5%+ in interest,” states Y Combinator’s company profile. That half-point reduction can translate to tens of thousands of dollars over a 30-year loan.

Chestnut is licensed in Texas and Colorado, with plans to expand rapidly into other U.S. states. For Aurora buyers, that means full regulatory compliance plus the speed advantages of an AI-first platform.

How does speed translate to real-world results?

- Pre-approval letters generated in under two minutes

- A 94% first-attempt approval rate

- Processing compressed from 30 to 45 days to minutes

When a rate jump threatens your deal, those numbers matter. A lender that can re-underwrite your file in hours instead of weeks gives you a realistic shot at closing on time.

Learn more about buying with Chestnut.

Chestnut’s fit for Aurora’s tight affordability

Aurora’s housing market is among the least affordable it has been in decades. “The affordability of purchasing a home in Aurora is at the lowest point in more than 20 years, nearly doubling in cost in the last eight,” reports the Common Sense Institute. Housing costs are outpacing income, so home affordability has decreased by 122% since 2013.

In that environment, every basis point counts. Chestnut’s AI technology consistently delivers approximately 0.50 percentage points below the national average 30-year fixed rate. For a borrower stretched by Aurora’s rising prices, that difference can mean qualifying for a home that would otherwise be out of reach, or freeing up hundreds of dollars a month for other expenses.

Take Control of Your Rate - Today

A mid-process rate jump does not have to end your homeownership plans. Federal and Colorado law protect your right to switch lenders before closing. Rate locks and float-downs offer some insulation, but when they fall short, pivoting to a faster, AI-powered lender can rescue the deal.

Here is what to remember:

- You can switch lenders anytime before signing final documents.

- Switching may involve repeat costs like appraisals, but long-term savings often outweigh them.

- Speed is critical: AI underwriting can compress weeks into minutes.

- Aurora’s affordability crunch makes every fraction of a percent valuable.

If your current lender cannot deliver the rate or timeline you need, Chestnut is licensed in Colorado and built to move fast. Explore how refinancing can save you money or start a new application today to see what rate you qualify for.

More Aurora and Arvada mortgage guides

- Best mortgage lender in Aurora CO: Chestnut vs 3 competitors (2026)

- How AI mortgage lenders in Aurora CO save borrowers 0.5% on rates

- Instant Mortgage Quote for Arvada Home Loans: Compare 100+ Lenders

- Real-Time Rate Monitoring for Arvada Home Loans: Lock at the Right Time

Frequently Asked Questions

Can I switch mortgage lenders in Aurora, CO before closing?

Yes, you can switch mortgage lenders at any time before signing the final loan documents. Both federal and Colorado laws protect your right to change lenders before closing.

What are the common reasons for switching mortgage lenders mid-process?

Common reasons include unexpected rate increases, poor customer service, delays in closing, and finding a better rate elsewhere. These factors can prompt borrowers to consider switching lenders to secure better terms.

How does a rate lock protect borrowers in Colorado?

A rate lock guarantees your interest rate for a specified period, protecting you from market fluctuations. However, if rates drop after locking, a float-down option might allow a one-time rate reduction, though it often comes with a fee.

What costs are associated with switching mortgage lenders?

Switching lenders may involve costs such as a new home appraisal, credit report fees, and potential rate-lock extension fees. It’s important to weigh these costs against the potential savings from a lower interest rate.

How does Chestnut Mortgage expedite the switching process?

Chestnut Mortgage uses AI-powered technology to streamline the mortgage process, offering rapid pre-approvals and reducing processing time from weeks to minutes. This efficiency can help borrowers meet tight closing deadlines.

Sources

- /news/how-chestnut-ai-can-cut-your-rate-in-a-rising-rate-market

- /news/how-to-find-the-best-mortgage-rates-this-month-may-2026

- https://www.ent.com/globalassets/pdf-files/legal/mortgage-rate-lock-disclosure-2025.pdf

- https://wtop.com/news/2024/12/can-you-switch-mortgage-lenders-before-closing/

- /news/how-mortgage-rates-work-and-how-to-get-the-best-one

- https://www.chase.com/personal/mortgage/education/financing-a-home/float-down-option

- https://www.rocketmortgage.com/learn/float-down-option

- https://www.freddiemac.com/pmms

- https://chestnutmortgage.com/compare-rates

- https://money.usnews.com/loans/mortgages/articles/can-you-switch-mortgage-lenders-before-closing

- https://dre.colorado.gov/sites/dre/files/documents/New%20MLO%20Handbook%202025.pdf

- https://www.consumerfinance.gov/ask-cfpb/what-happens-if-the-company-that-i-send-my-mortgage-payments-to-changes-en-215/

- /news/5-steps-to-get-preapproved-for-a-mortgage-fast

- https://coloradorealestatedigest.com/cost-of-home-appraisal-in-colorado/

- https://ycombinator.com/companies/chestnut

- https://hiretop.com/blog4/ai-mortgage-lender-chestnut-overview

- https://chestnutmortgage.com/buy

- https://www.commonsenseinstituteus.org/colorado/research/housing-and-our-community/aurora-co-housing-affordability-report

- /news/how-refinancing-can-save-you-money

Sources

Data and statistics referenced in this article are sourced from public mortgage industry reports and Chestnut's internal analysis.

Ready to find

your best rate?

Our automated quote flow is paused. Email contact@chestnutmortgage.com and the Chestnut team will help directly.