Mortgage lenders vs banks in Westminster CO: Which saves more?

When comparing mortgage lenders vs banks in Westminster CO, independent mortgage lenders typically save borrowers $1,000-$1,500 per loan through lower origination costs and digital efficiency. Banks offer convenience for existing customers but often charge higher fees, while credit unions consistently show the lowest costs overall among all lender types.

TLDR

• Westminster's median home price of $540,649 means closing costs range from $10,800-$27,000, making lender choice critical for savings

• Digital-first lenders cut origination costs by approximately $1,500 compared to traditional banks

• Credit unions offer the lowest average fees, while mortgage brokers typically charge the highest

• Westminster homes sell within 30 days on average, giving faster lenders a competitive advantage

• Colorado mortgage rates currently sit 30 basis points below national averages at 6.51% for 30-year fixed loans

• CHFA assistance programs provide up to $25,000 in zero-interest loans through participating lenders

Buying in Westminster? The question of mortgage lenders vs banks in Westminster CO isn't just academic—it can add or subtract thousands from your final bill. We'll unpack how each channel prices loans, where fees pile up, and why tech-driven lenders often edge out branch banks in Colorado's 2025 market.

Mortgage lenders vs. banks: what's the real difference?

Understanding who you're borrowing from matters just as much as the rate they quote you. The distinction shapes everything from your loan options to your closing costs.

Mortgage lenders specialize in real estate financing and can be a good option for applicants seeking access to diverse and competitive loan choices. Their entire business revolves around mortgages, which means dedicated underwriting teams, streamlined processes, and often more flexible approval criteria for borrowers with unique financial circumstances.

Banks offer a wider variety of financial products and services than mortgage lenders, but their mortgage options are often more limited and may be a better option for applicants who have an existing banking relationship. If you already bank with an institution, you might unlock loyalty discounts or fee waivers, but that convenience can come with trade-offs.

The revenue model differs too. Banks earn money across checking accounts, credit cards, and investment products, so mortgages represent just one profit center. Independent mortgage lenders live and die by their loan volume, creating stronger incentives to compete on price and close efficiently.

Common lender categories in 2025

Your lender list is likely to include five common types: national banks, regional and community banks, credit unions, mortgage brokers, and online-only mortgage lenders.

| Lender Type | Key Characteristics |

|-------------|--------------------||

| National banks | Broad product range; loyalty perks for existing customers |

| Regional/community banks | Local market knowledge; relationship-focused |

| Credit unions | Member-owned, tax-exempt; often lower fees |

| Mortgage brokers | Shop multiple lenders on your behalf |

| Online-only lenders | Competitive rates; digital-first experience |

Credit unions are non-profit financial institutions. Unlike banks, credit unions are owned by members and are exempt from federal taxes. That tax advantage often translates into lower rates and reduced fees for borrowers who qualify for membership.

Where do Westminster buyers save more—banks or mortgage lenders?

The numbers tell a compelling story. While individual experiences vary, systematic data reveals consistent patterns in who pays what.

Typically, you should be prepared to pay between 2% and 5% of the home purchase price in closing fees. On Westminster's median home price of roughly $540,000, that translates to $10,800 to $27,000, a range wide enough to demand serious comparison shopping.

Here's where lender type matters: average origination costs have gone up 35% over the past three years, putting pressure on borrowers across the board. However, technology adoption creates a significant split.

A Fannie Mae study of 1.1 million loans found that average total mortgage cost is about $7,200, or 3% of purchase price. But here's the critical detail: loans originated through mortgage brokers had higher lender fees, while those originated at credit unions had markedly lower costs.

The most efficient digital lenders are changing the equation entirely. The cost to originate a loan in Q3 2023 averaged approximately $11,600, but top performers cut that nearly in half.

Interest-rate spread in Colorado 2024-25

Colorado borrowers currently enjoy rates slightly below the national average. 30 Year Fixed Rate mortgages in Colorado averaged 6.51% for the week of 2025-04-24, compared to the national average of 6.81%, a 30 basis point advantage.

For Westminster specifically, today's mortgage rates are 6.827% for a 30-year fixed, 5.902% for a 15-year fixed, and 7.239% for a 5-year adjustable-rate mortgage. These figures represent averages; your actual rate depends on credit score, down payment, and which lender you choose.

Why does this matter for the bank-vs-lender question? Rate dispersion, the gap between the highest and lowest quotes, has widened significantly. That means the penalty for not shopping around has grown.

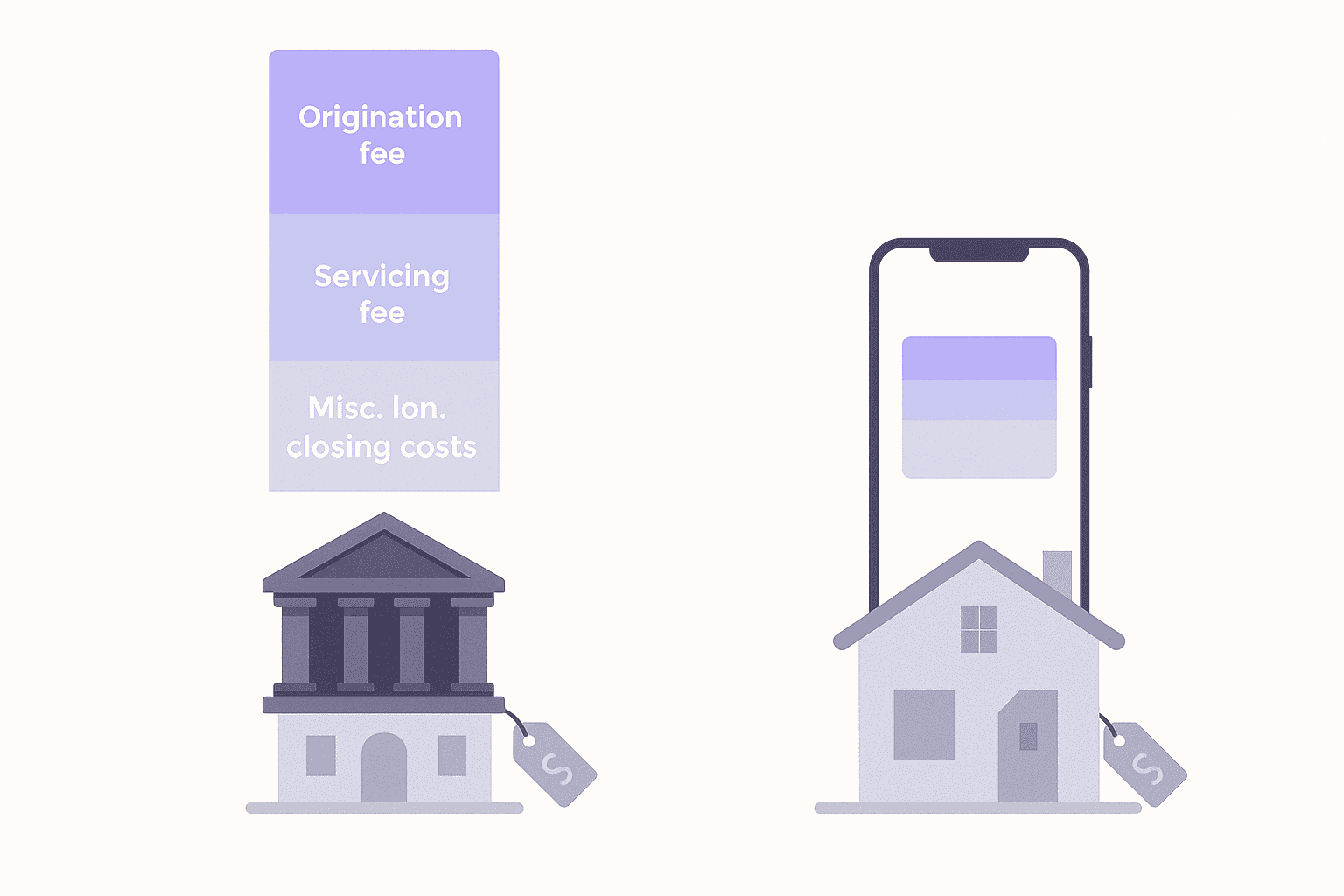

Origination & closing fees

Origination charges are upfront fees charged by your lender. Lender credits are rebates to offset your closing costs. This trade-off sits at the heart of comparing offers.

The technology gap creates a measurable cost difference. Lenders that utilize digital tools within LPA at higher rates originate loans that are $1,500, or 14%, less costly. Banks with extensive branch networks and legacy systems often struggle to match this efficiency.

Colorado's average closing costs are $5,713, landing in the middle of the national range. But that average masks significant variation based on your lender choice.

Key takeaway: Tech-forward independent lenders typically undercut traditional bank fees by $1,000 to $1,500 per loan through automation and streamlined operations.

Speed & customer experience: loan cycle times matter

Closing speed isn't just about convenience. Delays cost real money. Rate locks expire. Sellers grow impatient. Competing buyers with faster financing win deals.

The average closing cycle time for purchased mortgages has gradually decreased over the past four years from 46 days in 2016 to 40 days in 2019. But performance varies dramatically by lender type.

Independent mortgage banks consistently outpace their competition. The gap widens further when comparing top performers to laggards, the best lenders close 20 days faster than the slowest.

Scott Sheldon, a senior loan officer, describes the best-case scenario: "Three days. That's the fastest loan officer Scott Sheldon has ever seen someone get approved for a mortgage." More typically, he reports five to six days for underwriting approval and about 18 days for a commitment letter.

What enables this speed? Borrowers' top expectations of lenders are competitive interest rates, early certainty of approval, exceptional service, and assurance of on-time closing. Lenders who invest in technology deliver on all four.

The hidden ROI of a true pre-approval

Getting preapproved for a home loan isn't just a formality—it's your ticket to shopping with confidence. In Westminster's competitive market, where 70% of homes sell within 30 days, a solid pre-approval can mean the difference between winning and losing a bidding war.

A pre-approval that takes three days rather than three weeks provides several advantages:

Stronger offers: Sellers prefer buyers who've already cleared underwriting hurdles

Rate lock timing: Earlier approval means locking favorable rates before they rise

Negotiating leverage: Certainty of financing strengthens your position

Reduced stress: Knowing your exact budget before house hunting

Banks with slower processes put buyers at a disadvantage. When multiple offers compete, the buyer with faster, more certain financing often wins, even without the highest bid.

Who qualifies easier—and why that affects your wallet

Underwriting flexibility directly impacts your borrowing costs. Stricter criteria can push borrowers toward higher-rate loan products or require larger down payments.

The CHFA HomeAccess program offers assistance to first-time homebuyers in the form of a zero-interest second loan up to $25,000. Programs like this can dramatically reduce out-of-pocket costs, but only certain lenders participate.

Some local institutions advertise relaxed qualification requirements and incentives like closing-time guarantees. Yet eligibility restrictions and slower technology adoption can offset any headline savings for borrowers seeking efficient service.

Conforming loan limits also matter. The baseline loan limit value is $806,500 for a one-unit property, rising to $832,750 in 2026. Westminster's median home price of $540,649 falls comfortably within these limits, meaning most buyers can access conventional financing.

Colorado aid & credit-union perks banks rarely match

CHAC provides low interest, flexible loans to low and moderate income first time home buyers for down payment and closing cost assistance throughout Colorado.

Here's what's available:

Program | Amount | Terms |

|---|---|---|

CHAC down payment assistance | $5,000–$12,000 | 0%–5.5% APR; 12.5–30 year terms |

CHFA FirstGeneration | Up to $25,000 | Deferred repayment |

CHFA HomeAccess | Up to $25,000 | Zero-interest second loan |

These programs work through approved lenders, typically independent mortgage companies and credit unions rather than large national banks. The paperwork requirements and program rules favor lenders who specialize in these products.

How does Westminster's 2025 market tilt the scales?

The median home sold price in Westminster was $540,649 in March 2025, up 2.8% from last year. That modest appreciation, combined with slightly below-average Colorado rates, creates a favorable environment for buyers who shop strategically.

Westminster is currently a seller's market, meaning competition for homes remains intense. 70% of homes were sold within 30 days, underscoring the importance of financing that moves quickly.

Colorado-specific metrics paint a more complete picture:

Average originated loan amount: $491,000 (vs. national average of $369,000)

Serious delinquency rate: 1.14% (vs. national 1.57%)

Median principal & interest payment: $2,898 (vs. national $2,190)

Those higher loan amounts and payments mean the percentage savings from choosing the right lender translate into larger dollar amounts. A 0.25% rate reduction saves more on a $491,000 loan than on a $369,000 national average loan.

Today's mortgage rates in Westminster, CO are 6.827% for a 30-year fixed. But here's what matters more: the spread between lenders. Shopping multiple quotes, especially comparing banks against independent lenders, can yield savings of $600 to $1,200 annually.

How does Chestnut's AI platform stack up?

At Chestnut, we use proprietary technology to speed up mortgage preapproval, cutting through the usual delays. This matters in Westminster's fast-moving market, where homes go under contract in two weeks.

The technology advantage is measurable. Remember that lenders utilizing digital tools originate loans that are $1,500 less costly? Chestnut builds on this foundation with AI that compares offers from over 100 lenders to find competitive rates.

Price is not always king; customer experience is a real differentiator. First-time home buyers consistently rank experience higher than pricing when choosing a lender. Chestnut addresses both, competitive rates delivered through a streamlined digital process.

For Westminster buyers weighing their options, an AI-powered independent lender offers:

Faster pre-approvals than traditional bank timelines

Access to multiple wholesale rate sources

Lower overhead costs passed along as savings

Digital document handling that eliminates delays

Key takeaways for Westminster borrowers

The data points toward a clear conclusion: independent mortgage lenders, especially those leveraging technology, typically outperform traditional banks on both cost and speed for Westminster homebuyers.

Here's what to remember:

Shop multiple lenders. Rate dispersion has increased, making comparison shopping more valuable than ever.

Consider credit unions and independent lenders. They consistently show lower fees than banks and mortgage brokers in large-scale studies.

Prioritize pre-approval speed. In Westminster's 30-day average sale cycle, slow financing loses deals.

Explore Colorado assistance programs. CHFA and CHAC offer substantial help, but work through participating lenders.

Factor in technology. Digital-first lenders save roughly $1,500 per loan on origination costs.

Chestnut's tech keeps it manageable. We analyze your options to secure lower rates and trim unnecessary fees, exactly what Westminster buyers need in today's competitive market.

Ready to see what rates you qualify for? Start with Chestnut's instant quote tool to compare your options in under two minutes.

Frequently Asked Questions

What are the main differences between mortgage lenders and banks?

Mortgage lenders specialize in real estate financing, offering diverse loan options and streamlined processes. Banks provide a wider range of financial services but may have limited mortgage options. Mortgage lenders often have more competitive rates due to their focus on loan volume.

How do closing costs compare between banks and mortgage lenders in Westminster, CO?

Closing costs typically range from 2% to 5% of the home purchase price. Mortgage lenders, especially those using digital tools, often have lower origination and closing fees compared to traditional banks, saving borrowers $1,000 to $1,500 per loan.

Why is pre-approval speed important in Westminster's housing market?

In Westminster's competitive market, where 70% of homes sell within 30 days, fast pre-approval can give buyers an edge. It allows for stronger offers, better rate locks, and increased negotiating leverage, often leading to successful bids even without the highest offer.

What role does technology play in mortgage lending costs?

Technology significantly reduces mortgage lending costs. Lenders using digital tools can cut origination costs by up to 14%, translating to savings of approximately $1,500 per loan. This efficiency benefits borrowers through lower fees and faster processing times.

How does Chestnut Mortgage's AI platform benefit Westminster homebuyers?

Chestnut Mortgage uses AI to expedite pre-approvals and compare offers from over 100 lenders, ensuring competitive rates. This technology advantage helps Westminster buyers secure lower rates and reduce unnecessary fees, crucial in a fast-moving market.

Sources

https://sf.freddiemac.com/docs/pdf/cost-to-originate-full-study-2024.pdf

https://wellsfargo.com/mortgage/learn/compare-mortgage-lenders

https://myhome.freddiemac.com/blog/homebuying/what-are-closing-costs-and-how-much-will-i-pay

https://www.nerdwallet.com/mortgages/mortgage-rates/colorado/westminster

https://www.consumerfinance.gov/owning-a-home/compare/compare-loan-estimates/

https://sf.freddiemac.com/docs/pdf/fact-sheet/mortgage-cycle-time-benchmark-study.pdf

https://www.cbsnews.com/news/how-long-does-it-take-to-get-approved-for-a-mortgage/