Jumbo mortgage rates for $1.2M Austin homes: Best APRs in 2025

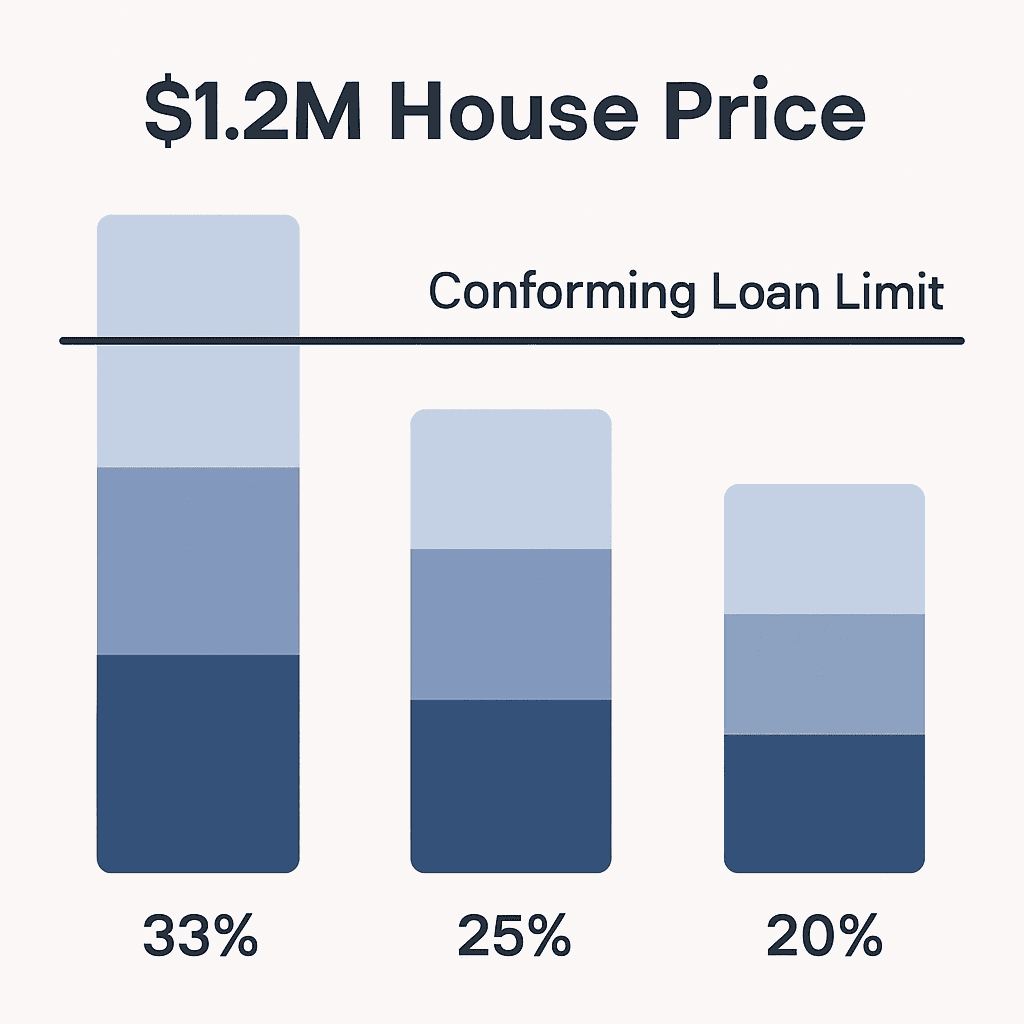

For Austin buyers seeking $1.2 million homes, jumbo mortgage rates currently average 6.44% nationally, though major banks often quote 6.5%-7.5%. With Texas's conforming loan limit at $806,500 for single-family homes, most purchases at this price point require jumbo financing unless buyers bring substantial down payments exceeding 33%.

At a Glance

• National jumbo rates average 6.44% for 30-year fixed mortgages, with 15-year options at 6.29%

• Austin's major banks typically quote at the higher end of the 6.5%-7.5% range seen in recent months

• Minimum requirements include 680+ credit score, 10-20% down payment, and 6-12 months of mortgage payments in reserves

• Shopping five lenders can save approximately $3,000 over the loan lifetime

• Non-bank lenders and AI-powered platforms often beat traditional bank quotes by 0.25-0.50 percentage points

Purchasing a $1.2 million home in Austin means navigating the jumbo mortgage landscape, where current rates sit near 6.44% nationally while Austin's major banks often quote at the higher end of this range. With rates ranging 6.5%-7.5% in recent months, understanding how to secure competitive financing has become crucial for Austin homebuyers entering the luxury market.

2025 jumbo mortgage rates in Austin at a glance

The latest data shows jumbo mortgage rates have stabilized but remain elevated compared to historical averages. "As of Wednesday, November 19, 2025, the national average 30-year fixed jumbo mortgage interest rate is 6.44%, up compared to last week's of 6.42%," according to recent rate tracking. For Austin specifically, buyers should expect to see quotes near or above these national benchmarks when approaching traditional lending institutions.

The term "jumbo loan" refers to any mortgage exceeding conforming loan limits set by the Federal Housing Finance Agency. While these loans once carried significantly higher rates than conforming mortgages, the gap has narrowed considerably. Today's jumbo borrowers face a more competitive landscape, though securing the best rates still requires strategic shopping and strong financial credentials.

Looking ahead through 2025, market conditions suggest continued volatility. Federal Reserve policy decisions and broader economic indicators will influence rate movements, making timing and lender selection increasingly important for Austin's luxury homebuyers.

Is a $1.2 million Austin purchase automatically a jumbo loan?

Not necessarily. The answer depends on your down payment amount and Travis County's conforming loan limits. The 2025 limit stands at $806,500 for single-family homes throughout Texas, including Austin. This means a $1.2 million purchase with a 33% down payment ($396,000) would keep your loan amount at exactly $804,000—just under the conforming threshold.

However, most buyers putting less than one-third down will cross into jumbo territory. A traditional 20% down payment on a $1.2 million home results in a $960,000 loan, clearly exceeding conforming limits. Even with 25% down, you'd still need a $900,000 mortgage.

Texas maintains uniform conforming limits across all counties, unlike California or New York where high-cost area adjustments apply. Harris County follows the same $806,500 threshold as Travis County, keeping consistency across Texas's major metropolitan areas.

Key takeaway: Unless you're bringing substantial cash to closing, that $1.2 million Austin property will likely require jumbo financing.

How current jumbo APRs stack up: national averages vs. Austin's big banks

The jumbo mortgage rate landscape reveals significant disparities between national averages and what Austin's major banks actually quote. Here's the current snapshot:

Rate Type | National Average | Austin Bank Range | Spread |

|---|---|---|---|

30-Year Fixed Jumbo | 6.5% - 7.5% | +0.06% to +1.06% | |

Recent Daily Tracking | Upper band pricing | Typically at ceiling | |

Portfolio Loan Premium | Base rate | Bank-held premium |

Large financial institutions consistently price at the upper end of these ranges. Wells Fargo, Chase, and Bank of America—traditionally dominant in the jumbo space—often quote rates approaching 7% for standard jumbo scenarios. This pricing reflects their portfolio lending model, where loans remain on bank balance sheets rather than being sold to secondary markets.

The data shows Thursday's jumbo 30-year rate at 6.46%, yet Austin borrowers frequently encounter quotes 50 to 100 basis points higher from major banks. This premium particularly impacts borrowers who default to their existing banking relationships without comparing alternatives.

Why big banks quote higher jumbo rates -- and who's filling the gap

The structural reasons behind inflated bank pricing stem from how these institutions handle jumbo loans. Many banks keep jumbos as portfolio loans, tying up capital that could otherwise generate returns through other lending activities. This capital constraint, combined with heightened regulatory requirements following 2023's regional banking turmoil, drives banks to price defensively.

Meanwhile, the mortgage landscape has shifted dramatically. Independent mortgage companies now originate nearly 70% of purchase loans, up from 62.1% in 2020. These non-bank lenders operate with different economics—they sell loans rather than holding them, enabling more aggressive pricing to win market share.

"Jumbo mortgages don't get sold to Fannie or Freddie," notes Melissa Cohn, regional vice president of William Raveis Mortgage. "Many of them are portfolio loans", meaning banks shoulder the full risk rather than distributing it through securitization. This risk retention translates directly into higher rates for borrowers who stick with traditional banking channels.

The gap creates opportunities for borrowers willing to explore beyond their primary bank. Non-bank lenders, credit unions, and fintech platforms increasingly compete for jumbo business with rates closer to national averages.

How Austin buyers can lock a lower jumbo APR in 2025

Securing competitive jumbo rates requires a systematic approach that goes beyond accepting your bank's first offer. Start by pulling quotes from at least five different lender types:

Regional credit unions (often member-restricted but worth joining)

Independent mortgage companies

Online-first lenders

Portfolio lenders specializing in jumbo products

AI-powered platforms that aggregate multiple offers

Timing matters significantly. Rate shopping saves $1,500 with just one additional quote, while comparing five lenders typically saves $3,000 over the loan's lifetime. For a $960,000 jumbo loan, even a 0.25% rate reduction saves approximately $145 monthly—nearly $52,000 over 30 years.

Consider these strategic moves:

Lock when the 10-year Treasury dips below 4.3%

Explore 15-year terms if cash flow permits (currently averaging 6.29%)

Negotiate lender credits to offset closing costs

Bundle banking relationships for relationship pricing

Use AI comparison tools to access wholesale rates

The most successful borrowers treat rate shopping like negotiating a car purchase—never accepting the sticker price and always maintaining multiple options until closing.

Chestnut AI™ vs. manual rate shopping

Chestnut's proprietary AI technology fundamentally changes how borrowers access competitive jumbo rates. Rather than manually contacting individual lenders, the platform instantly analyzes options across more than 100 lending sources, consistently delivering rates approximately 0.50 percentage points below market averages.

The technology advantage shows in the numbers. AI-based underwriting reduces processing time from the typical 30-45 days to just eight minutes. "Borrowers using Chestnut AI™ typically see rate savings of 0.5% or more compared to traditional shopping methods," with instant quotes in under two minutes rather than days of phone calls and paperwork.

This efficiency particularly benefits jumbo borrowers, who often face more complex underwriting requirements. The AI system identifies lenders with specific appetites for high-value Austin properties, matching borrower profiles to optimal lending programs that manual searches might miss.

Eligibility checklist for a $1.2 M jumbo loan in Texas

Qualifying for a jumbo mortgage requires meeting stricter standards than conforming loans. Here's what Texas lenders typically require:

Credit Score Requirements:

700+ for best rates

740+ for maximum loan amounts

Down Payment Thresholds:

Some programs accept 10% with higher credit scores

5% options available up to $1.5M with 680+ credit

Debt-to-Income Limits:

Maximum 45% DTI for most lenders

Some flexibility with compensating factors

Lower ratios improve rate pricing

Cash Reserves:

6-12 months of mortgage payments in liquid assets

Higher reserves for investment properties

Retirement accounts typically count at 70% value

Documentation Requirements:

W-2s or 1099s for income verification

Complete asset statements

Self-employed need business financials

Texas-specific programs offer some flexibility. New 2025 options allow 5% down on jumbos up to $1.5 million with 680 credit scores, expanding access for qualified buyers with less cash on hand.

How rate volatility and the lock-in effect shape Austin prices

The mortgage rate environment profoundly impacts Austin's luxury housing market through what economists call the "lock-in effect." Research shows each percentage point increase in the rate differential between current markets and existing mortgages reduces home sale probability by 18.1%.

This dynamic has real consequences. The lock-in effect drove home prices up 7.0% while simultaneously reducing transaction volume by an estimated 1.72 million sales nationally from 2022 to 2024. Austin's high-end market feels this acutely—owners with sub-4% mortgages from 2020-2021 resist selling into today's 6.5% environment.

For buyers, this creates a paradox. Limited inventory pushes prices higher even as elevated rates reduce purchasing power. A $1.2 million home financed at 6.5% costs approximately $1,400 more monthly than the same purchase at 4.5%—a $504,000 difference over 30 years.

Inflation concerns add another layer of complexity. "Mortgage rates spiked following the release of January's consumer price index report, which showed that inflation rose more than expected to 3% annually," notes recent analysis. This suggests the Federal Reserve will maintain its cautious approach to rate cuts, keeping jumbo rates elevated through 2025.

Key takeaways for Austin jumbo borrowers in 2025

Austin's $1.2 million home buyers face a challenging but navigable jumbo mortgage landscape. Big banks consistently quote at the upper end of the 6.5%-7.5% range, but savvy borrowers who compare multiple lenders can access rates closer to the 6.44% national average.

The most important actions for securing competitive jumbo financing:

Compare at least five lenders including non-bank options

Prepare strong financials with 680+ credit and 20% down

Time your application strategically with market conditions

Consider AI-powered platforms that aggregate wholesale rates

Chestnut's technology has proven particularly effective, consistently delivering approximately 0.50 percentage points below market averages through its network of over 100 lenders. For a $960,000 jumbo loan, this half-point advantage translates to roughly $290 monthly savings—over $104,000 across the loan's lifetime.

As 2025 progresses, the gap between bank-quoted rates and competitive market rates will likely persist. Austin buyers who treat jumbo financing as a competitive marketplace rather than accepting their bank's first offer position themselves to save tens of thousands over their loan term. The tools exist to beat inflated bank rates—success comes down to using them strategically.

Frequently Asked Questions

What is the current national average for jumbo mortgage rates?

As of November 19, 2025, the national average 30-year fixed jumbo mortgage interest rate is 6.44%, slightly up from the previous week's 6.42%.

How do Austin's jumbo mortgage rates compare to national averages?

Austin's major banks often quote jumbo mortgage rates between 6.5% and 7.5%, which is higher than the national average of 6.44%.

What factors influence jumbo mortgage rates in Austin?

Jumbo mortgage rates in Austin are influenced by Federal Reserve policies, economic indicators, and the lending practices of major banks, which often price at the higher end due to portfolio lending models.

How can Austin homebuyers secure lower jumbo mortgage rates?

Austin homebuyers can secure lower jumbo rates by comparing quotes from at least five different lenders, including non-bank options, and using AI-powered platforms like Chestnut to access competitive rates.

What are the eligibility requirements for a jumbo loan in Texas?

To qualify for a jumbo loan in Texas, borrowers typically need a minimum credit score of 680, a 20% down payment, a maximum 45% debt-to-income ratio, and 6-12 months of cash reserves.

How does Chestnut's AI technology benefit jumbo mortgage borrowers?

Chestnut's AI technology provides borrowers with instant quotes from over 100 lenders, often delivering rates approximately 0.50 percentage points below market averages, significantly reducing borrowing costs.

Sources

https://cnet.com/personal-finance/compare-jumbo-mortgage-rates

https://www.usdamortgagesource.com/blog/texas-jumbo-home-financing-updates/

https://www.fhamortgagesource.com/understanding-jumbo-home-loans-in-houston-2025-edition/

https://www.investopedia.com/the-best-jumbo-mortgage-rates-11733500

https://money.usnews.com/loans/rates/mortgages/jumbo-mortgage

https://www.housingwire.com/articles/the-jumbo-market-is-up-for-grabs-part-ii/

https://chestnutmortgage.com/resources/chestnut-ai-delivers-0-50-point-rate-advantage-2025

https://chestnutmortgage.com/resources/how-chestnut-ai-can-cut-your-rate-in-a-rising-rate-market