Who Compares 100+ Lenders for Fort Collins Home Loans?

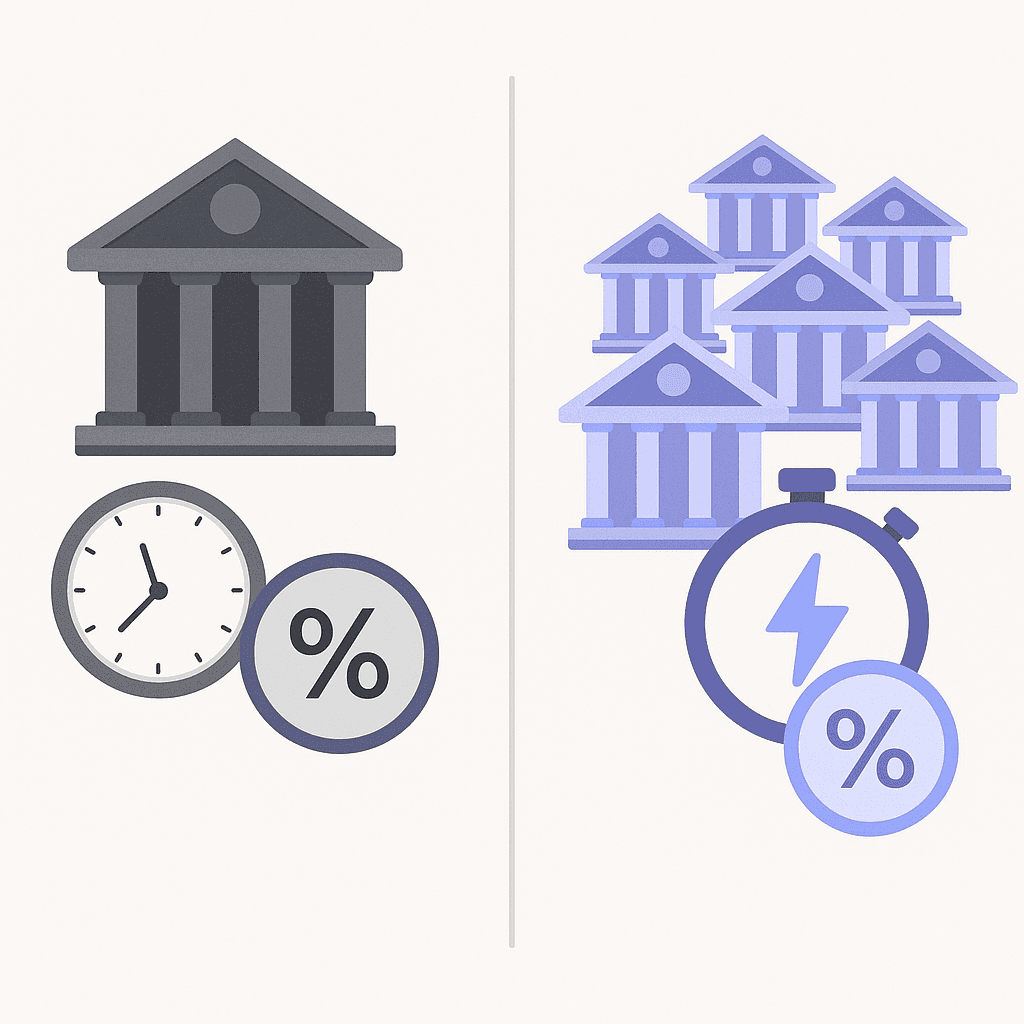

Chestnut Mortgage uses AI technology to compare rates from over 100 lenders simultaneously, while traditional lenders typically check only 1-5 sources from their own rate sheets or limited wholesale partners. This comprehensive comparison delivers 0.5% average rate savings and provides instant quotes in under two minutes, far exceeding the scope of single-bank shopping that most Fort Collins borrowers still rely on.

TLDR

• Traditional lenders quote from their own products or 1-5 wholesale partners, limiting borrower options and potentially costing thousands in extra interest

• Chestnut's AI engine analyzes options across more than 100 lenders in real-time, delivering comprehensive market coverage

• The platform provides instant rate comparisons in under 2 minutes versus days with traditional shopping methods

• Technology-driven comparison typically yields 0.5% or more in rate savings compared to single-lender quotes

• Direct API integrations and soft credit pulls enable safe, comprehensive shopping without multiple hard inquiries

Most buyers shopping for Fort Collins home loans still rely on a single bank quote - even though studies show checking just three offers can shave thousands off lifetime interest. According to survey data, half of US mortgage borrowers seriously considered only one lender, and just 3 percent looked at more than three. This post explains why comparing 100+ lenders is now possible, how it works, and what it means for your wallet.

Why Casting a Wider Net Matters When Financing a Fort Collins Home

The mortgage market rewards shoppers. According to the National Survey of Mortgage Originations, half of borrowers only seriously considered one lender, leaving substantial savings on the table. The Consumer Financial Protection Bureau puts it bluntly: "Borrowers who shop around can save thousands of dollars." Freddie Mac research confirms that homebuyers who apply to multiple lenders can save $600 to $1,200 annually.

Why do so few people compare? Time, complexity, and the misconception that rates are roughly the same everywhere. In reality, identical borrowers can receive offers that vary by more than half a percentage point on the same day - a gap that compounds into tens of thousands of dollars over a 30-year loan.

Key takeaway: Casting a wider net consistently translates into lower lifetime costs, yet most borrowers stop searching far too soon.

Why Do Most Lenders Only Check 1-5 Sources, and How Does That Hurt Borrowers?

Traditional lenders - banks, credit unions, and many online platforms - typically quote from their own rate sheet or a handful of wholesale partners. Research from the Philadelphia Fed finds that the difference between the 90th and 10th percentile interest rate for identical borrowers is over 50 basis points. That gap can translate to roughly $6,250 in upfront cost on a typical $250,000 loan, according to the same study.

Several structural factors limit traditional shopping:

Capacity constraints: Manual underwriting and phone-based processes can only handle so many comparisons.

Investor relationships: Retail lenders earn margin by selling to a small roster of investors; expanding that roster adds operational overhead.

Market power of large lenders: Philadelphia Fed researchers note that the largest lenders tend to charge higher rates and exhibit the most price dispersion, suggesting they profit from borrowers who don't shop.

MyFICO analysis reinforces the point: mortgage borrowers in the second half of 2022 who received as many as five rate quotes could have saved over $6,000. Meanwhile, Realtor.com data shows an 86-basis-point spread between the least and most expensive lenders - the single largest controllable factor in a borrower's rate.

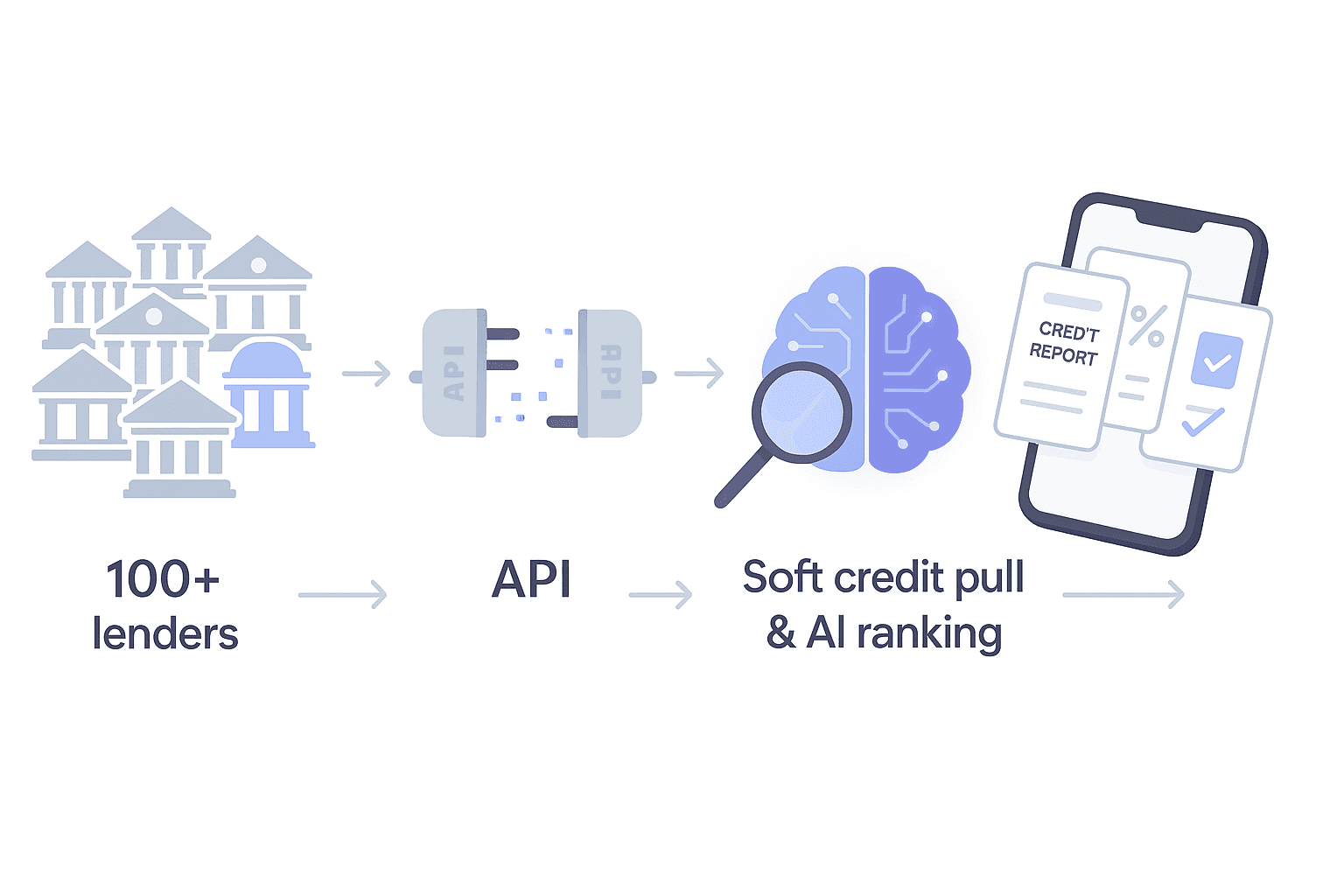

How Chestnut AI Compares 100+ Lenders in Real Time

Chestnut Mortgage addresses the shopping gap with technology. As the company's own documentation states, "Chestnut AI™ analyzes options across more than 100 lenders in real-time."

Here is how the process works:

Direct API integrations: Chestnut maintains live data feeds with banks, credit unions, and wholesale investors. Pricing engines like Mortech handle thousands of mortgage offer requests per day, returning lender-specific quotes in seconds.

Instant soft-pull credit analysis: The platform pulls a tri-merge credit report without affecting your score, then matches your profile against eligibility rules across the full lender network.

AI-driven ranking: Proprietary algorithms weigh rate, fees, and lender reliability to surface the best executable options. Fannie Mae's Loan Pricing API - used industry-wide - combines asset price, servicing premiums, and loan-level adjustments into a single transparent response, enabling the kind of apples-to-apples comparison that manual shopping rarely achieves.

The result: borrowers see comprehensive rate comparisons in under two minutes, far beyond what a single bank visit could deliver.

Speed, Savings, and Certainty: Measurable Gains from a 100-Lender Search

Quantifying the upside helps put Chestnut's model in perspective.

Metric | Traditional Shopping | Chestnut AI |

|---|---|---|

Lenders compared | 1-5 | 100+ |

Time to quote | Days | Under 2 minutes |

Typical rate advantage | Baseline | ~0.5% lower |

Chestnut reports that borrowers using its AI engine typically see rate savings of 0.5% or more compared to traditional methods. Freddie Mac research supports this magnitude: borrowers who received multiple quotes in late 2022 could have saved more than $6,000 over the life of the loan, assuming a five-year hold.

Operational efficiency matters, too. A 2024 Freddie Mac study found that average origination costs have risen 35% over the past three years. Digital-first lenders that leverage automated tools can cut per-loan costs by roughly $1,500, savings that often flow through to borrowers in the form of lower fees or better pricing.

How Do APIs, AI, and RESPA Safeguards Enable Safe 100-Lender Shopping?

Behind the scenes, several technologies and regulations make mass comparison both fast and fair.

APIs and Pricing Engines

Application programming interfaces connect lenders, secondary-market investors, and consumer platforms. Fannie Mae's Loan Pricing API, for example, consolidates asset price, servicing released premiums, and loan-level price adjustments into one call. Enterprise pricing engines built on NoSQL databases can return quotes 5-10x faster than older systems and support multiple intraday price updates.

RESPA Section 8 and Neutral Presentation

The Consumer Financial Protection Bureau has made clear that digital comparison platforms must present lenders based on neutral criteria rather than compensation. Platforms that steer consumers toward higher-paying participants violate the Real Estate Settlement Procedures Act. This rule ensures that when you see a ranked list of offers, it reflects objective factors - rate, fees, eligibility - not hidden payments.

AI Underwriting and Valuation Standards

Automated valuation models used in credit decisions must meet quality-control standards mandated by the Dodd-Frank Act, including nondiscrimination testing and random-sample audits. These safeguards help ensure that algorithmic lending expands access without introducing bias.

Fort Collins Housing Snapshot: Why Every Basis Point Counts in 2025

Fort Collins remains a competitive market. According to Realtor.com data, the median listing price is $597,000 as of September 2025, with properties spending a median of 64.5 days on the market. Rocket Homes reports the median sold price at $565,013 (May 2024), up 2.7% year-over-year, and notes that 35.8% of homes sold above asking price.

NerdWallet's May 2025 snapshot shows Fort Collins buyers facing a national average 30-year fixed APR of 7.001%. On a $500,000 loan, a 0.5-percentage-point rate reduction - the typical Chestnut advantage - translates to roughly $150 per month, or more than $50,000 in interest over 30 years.

Key takeaway: In a market where prices remain elevated and inventory is tight, securing the lowest possible rate is one of the few levers buyers can pull.

How to Compare Lenders Without Dinging Your Credit or Sanity

A common myth holds that shopping multiple lenders will tank your credit score. In reality, the CFPB confirms that within a 45-day window, multiple lenders can check your credit without additional impact. Newer FICO models extend the rate-shopping window to 45 days, treating all mortgage inquiries in that period as a single event.

Here is a practical checklist:

Gather documents first: Pay stubs, tax returns, and bank statements speed every application.

Request Loan Estimates from at least three lenders: The CFPB notes that homebuyers can save $600 to $1,200 per year by comparing offers.

Use soft-pull platforms when possible: Chestnut's initial quote uses a soft pull, so you can explore options before committing to a hard inquiry.

Negotiate with competing estimates in hand: The CFPB advises that your best bargaining chip is usually having Loan Estimates from other lenders.

Chestnut vs. Fort Collins Lenders: Who Really Delivers More Options?

Fort Collins buyers have no shortage of local and national lenders. Guild Mortgage, for instance, is one of the top 10 independent mortgage lenders in the nation and offers down payment assistance, jumbo, conventional, FHA, VA, USDA, and renovation loans. Movement Mortgage markets underwriting results within six hours and a seven-day processing target, though its quotes still draw from a limited product shelf.

Yet these lenders share a structural limitation: they quote from their own product shelf or a modest set of investor relationships. Bankrate notes that Guild Mortgage finished slightly below average for customer satisfaction in J.D. Power's most recent rankings, and the lender doesn't disclose mortgage rates unless you contact a loan officer. That opacity makes apples-to-apples comparison difficult.

Chestnut's 100-lender network sidesteps these constraints. Because the platform pulls live pricing from banks, credit unions, and wholesale investors simultaneously, borrowers see the full market - not just one institution's view of it. The result is greater pricing transparency and, in most cases, a measurably lower rate.

The Bottom Line on Securing the Best Fort Collins Home Loan

Shopping around has always mattered, but technology now makes it effortless. Where previous generations compared a handful of quotes over weeks, Chestnut's AI engine delivers side-by-side offers from more than 100 lenders in under two minutes - often shaving half a percentage point off the rate.

In a Fort Collins market defined by $600,000 median prices and 7%-plus mortgage rates, that difference compounds into real money: lower monthly payments, faster equity growth, and tens of thousands saved over the life of the loan.

Ready to see what 100-lender comparison looks like? Get a free quote from Chestnut and discover what rate you actually qualify for - before you commit to a single bank's offer.

Frequently Asked Questions

Why is it important to compare multiple lenders for a home loan?

Comparing multiple lenders can lead to significant savings on interest rates and fees. Studies show that borrowers who shop around can save thousands of dollars over the life of their loan.

How does Chestnut Mortgage compare 100+ lenders?

Chestnut Mortgage uses AI technology and direct API integrations to analyze options from over 100 lenders in real-time, providing comprehensive rate comparisons in under two minutes.

What are the benefits of using Chestnut's AI for mortgage comparisons?

Chestnut's AI offers faster quotes, typically under two minutes, and can save borrowers around 0.5% on interest rates compared to traditional methods, translating to significant savings over the loan's lifetime.

How does shopping around affect my credit score?

Within a 45-day window, multiple credit checks for mortgage rates are treated as a single inquiry, minimizing the impact on your credit score.

What makes Chestnut different from traditional lenders?

Unlike traditional lenders that offer limited quotes, Chestnut provides a broader market view by comparing offers from over 100 lenders, ensuring more competitive rates and greater transparency.

Sources

https://www.philadelphiafed.org/-/media/frbp/assets/working-papers/2024/wp24-11.pdf

https://gflec.org/wp-content/uploads/2019/04/Bhutta-Neil-V2-1.pdf

https://www.consumerfinance.gov/owning-a-home/explore/contact-multiple-lenders/

https://www.realtor.com/research/aug-2024-mortgage-determinants/

https://sf.freddiemac.com/docs/pdf/cost-to-originate-full-study-2024.pdf

https://www.rockethomes.com/real-estate-trends/co/fort-collins

https://www.nerdwallet.com/mortgages/mortgage-rates/colorado/fort-collins

https://www.consumerfinance.gov/owning-a-home/compare/request-and-review-multiple-loan-estimates/

https://www.consumerfinance.gov/owning-a-home/compare/compare-loan-estimates/